How to Avoid CAA Liability: A Case Study

By Al Lewis

Prior to 2023, vendor misstatements of outcomes were only of academic interest to folks like the Validation Institute, and to purchasers who prioritized management of their healthcare spending in practice, rather than just as a talking point. However, the Consolidated Appropriations Act changes everything. Today, significant penalties await those who pay vendors who claim illegitimate outcomes.

How can you tell the difference? If a vendor’s outcomes are legitimate, they get validated by the Validation Institute. If not, they oxymoronically “pay independent actuaries” to validate them. (A vendor with legitimate outcomes may also pay actuaries who work for a benefits consulting firm, because they want to curry favor with that benefits consulting firm.)

You might ask: “Doesn’t the Validation Institute also get paid by the vendor?[1] So how are they independent?” The bright-line difference: the Validation Institute (VI) offers a unique Credibility Guarantee: if a validation is inaccurate, a third-party arbitration process can award a large multiple of VI fees to the party making the claim of inaccuracy. There is the reputational issue as well. If VI got the reputation for putting its finger on the scale, no vendor would bother. Whereas if a large consulting firm gets the reputation that it will “show savings,” vendors will sign up and broadcast the result.

That is exactly what happened in the case study below.

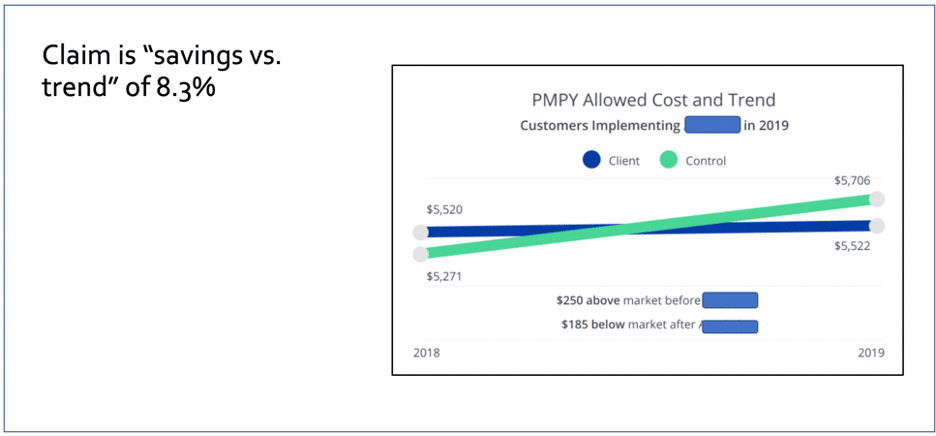

By way of background, a major vendor paid a major actuarial firm to claim that the vendor had achieved an 8.3% reduction in claims costs, by providing care navigation/advocacy services to employees who needed to significantly access the healthcare system, due to having a myriad of serious healthcare issues. These are the small number of multiple comorbid folks who drive up your costs, and if you can control their costs, you can enjoy savings for your healthspend as a whole.

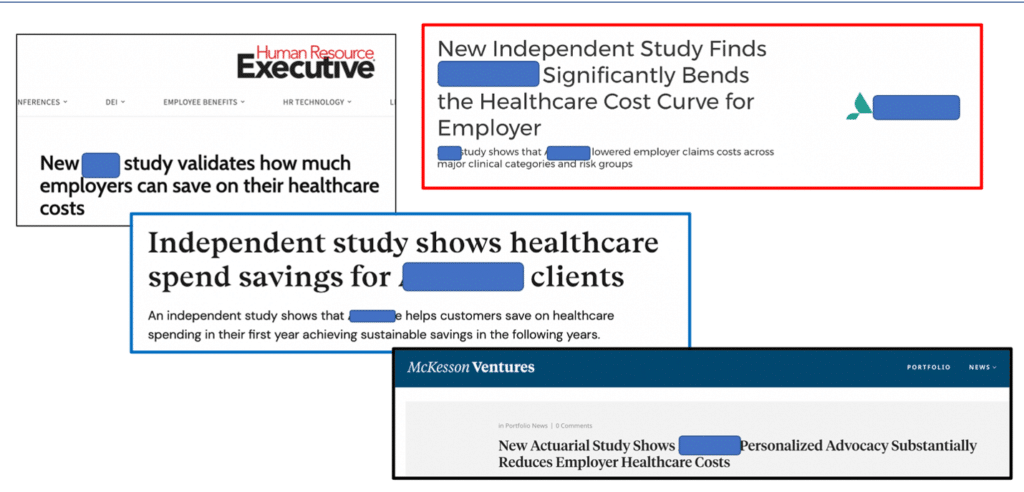

Because major names were involved and a major PR effort was launched, they got a fawning press to regurgitate every word, including “independent” twice:

And indeed in every single category of condition, they saved money. This includes “mental mood” and “mental anxiety,” presumably as distinguished from physical mood and physical anxiety. Speaking of physical issues, they made dramatic improvements in hypothyroidism and even cancer. Why use an endocrinologist or oncologist when you can call someone on the phone? They even save money in “esophageal.” Maybe it’s just me, but if my esophagus were acting up, I suspect I would contact my doctor.

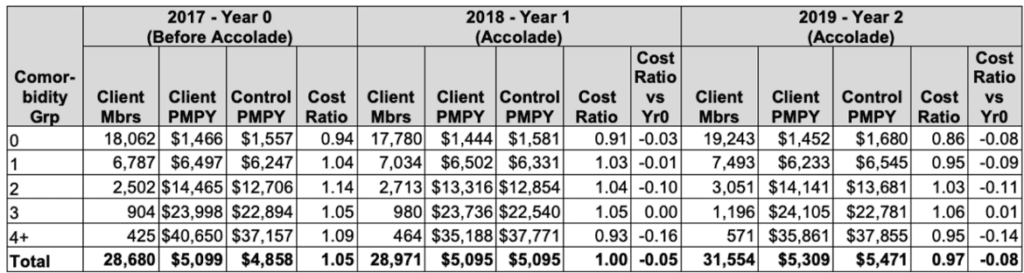

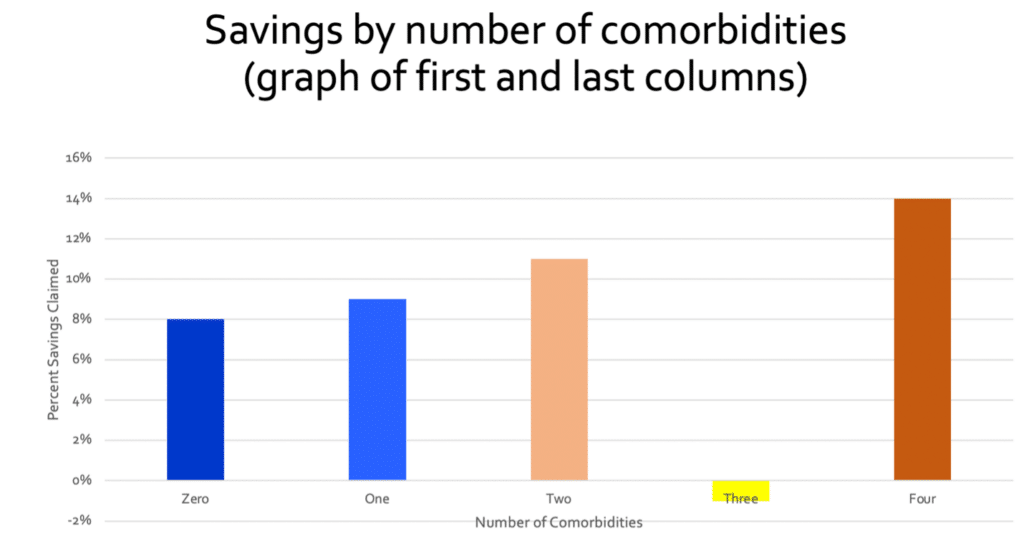

They helpfully provided the raw cost data by comorbidity group. This gives the triple-digit IQ crowd, of which I am a member, a chance to read it, as opposed to just reading the headlines. They separated the groups by comorbidity into 5 categories, and then added the savings in each of the 5 categories in the rows in the right-hand column, and then divided by 5. That yields a “Cost Ratio vs. Yr0,” of “-0.08,” or what people not qualified to be actuaries would call “8% savings.” (Actually 8.3%, which they rounded down.)

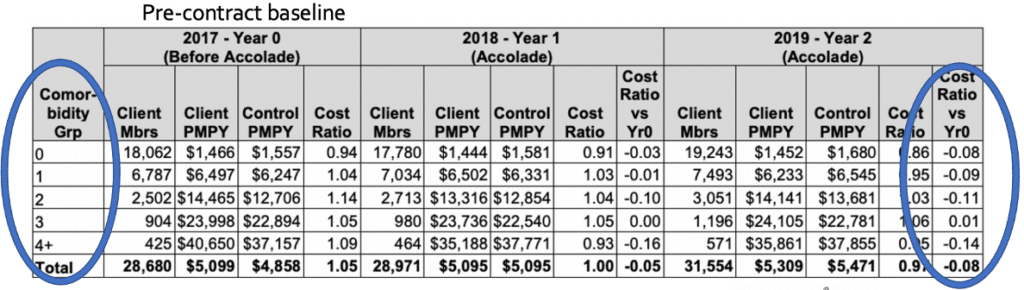

I’m not going to say this number is a deliberate lie. Perhaps these actuaries were simply absent the day in actuary college when the professor taught the module on averaging. That might be why they took a straight arithmetic average of those five right-hand figures instead of noticing in the first column the dramatically different numbers of “Client Mbrs” in each “Comorbidity Grp”:

Watch what happens if you do the analysis correctly.

Let’s make it very visual and use only short words, so that these actuaries can follow the logic. We’ll start by graphing the left-hand vs. the right-hand columns. Note that somehow the vendor’s magic, which works so well on people with 2 or 4 comorbidities, fails epically on people with exactly three comorbidities, but we’ll leave that anomaly for others to dissect:

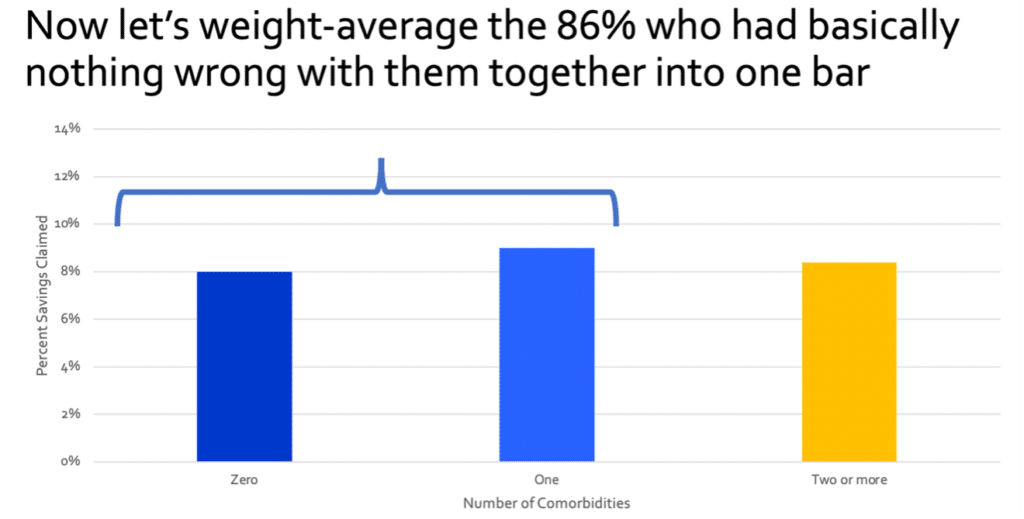

Now, let’s collapse the 3831 people (about 14% of the population) in Comorbidity Groups Two, Three and Four into one group of “multiply comorbid” members. But recalling our fifth-grade math, let’s weight-average those three subgroups based on the number of people in each group (2502 ,904, and 425 respectively in Groups Two, Three and Four), rather than just taking an arithmetic average of those three right-hand numbers.

These multiply comorbid people are the folks who might actually benefit from care advocacy, since they are accessing the healthcare system, and spending large amounts of money in it. This makes it possible, at least in theory, to save money by helping members “navigate” the system.

When you do that, the average savings for those groups becomes this beige bar below. Then, as you’ll note, we repeat the exercise for the groups with either nothing or almost nothing wrong with them. These groups would have very little if any reason to seek advocacy.

Weight-averaging those two groups allows us to then calculate the actual savings from care navigation from the multiply comorbid group, vs. the group that didn’t need care advocacy. (It is, of course, possible that a few people in the left-hand column below called in, perhaps because their esophagus was acting up and their doctor wasn’t sure what to do.)

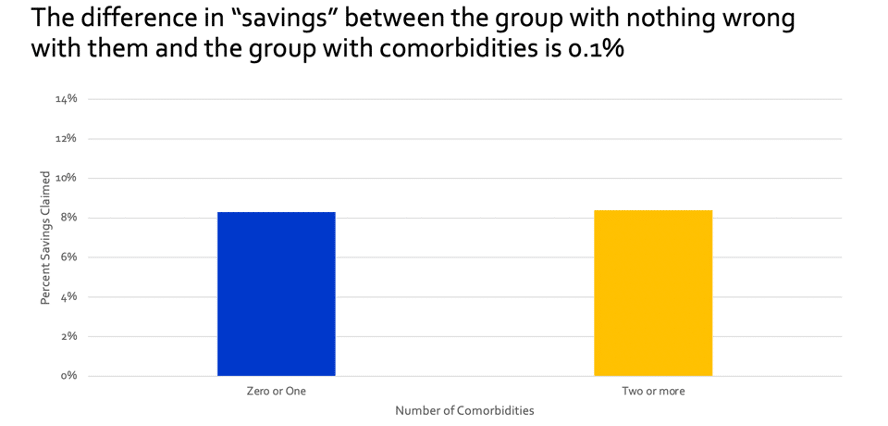

Conclusion: there was no meaningful distinction between the multiply comorbid group that could maybe have benefited from advocacy, and the group that didn’t. One of two other conclusions must be the case:

- The vendor saved lots of money even on people who:

- didn’t need that vendor’s services,

- perhaps didn’t even know that vendor existed, and

- likely never called in to get help with a health issue, preferring to talk to their doctor.

- Virtually all the “savings” was attributable to simply picking an inflated trend to measure against. That might also explain why every single condition category showed savings.

We would leave it to the reader to decide which is the case. I think the vendor and their actuaries are quite convinced the first conclusion is the correct one. Why do I suspect that? Easy. I pointed out this paradoxical outcome to them and they didn’t fix it. Obviously if it were a mistake, they would have fixed it. Right? Right?

The argument for #2 is that I also offered to bet them a million dollars that the second conclusion is correct. Their chief actuary viewed my Linkedin profile and declined, probably thinking that it wasn’t fair to take my money and impoverish me.

Hopefully for any employer using these people, the first conclusion is correct, and the actuary declining my offer was truly concerned about my financial well-being. Otherwise, they could get their customers in a lot of hot water. How’s that? Because it’s now illegal for an employer to retain vendors who fabricate their outcomes,under the Consolidated Appropriations Act, provided that you as an employer have reason to suspect the outcomes are fabricated – which, having read this far, you now do.

Specifically, this second case fails the standard of “meaningful, repeatable and unbiased proof” of providing “reasonable value.” If an employer is found in breach, then the employer’s leadership is personally liable to pay restitution to their employee health plan.

The vendor itself is not liable, which perhaps explains why these folks are still pushing these results hard, right on their homepage, upping the ante to “most rigorous independent study.”

On the other hand, recall that these folks do appear to have a cost-effective remedy for esophageal problems. That’s good news. Why? Because anyone who claims they believe these results would first have to swallow very, very hard.

[1] Oftentimes either the employer pays, or the employer compels the vendor to pay, to be VI-validated.